2026–27 Federal Budget Proposals: Key Tax Reform Measures Explained

Treasurer Jim Chalmers handed down the 2026–27 Federal Budget on 12 May 2026, announcing a range of proposed tax reforms affecting employees, investors, and businesses.

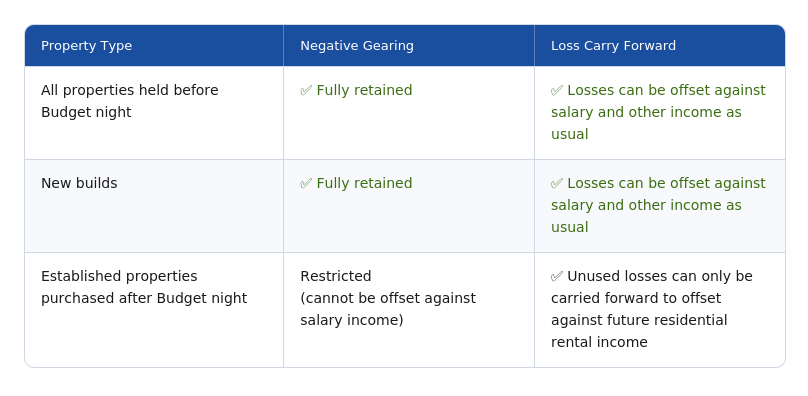

1. Negative Gearing Reform

The Government proposes to limit negative gearing concessions to newly built residential properties from 1 July 2027, with the aim of encouraging additional housing supply.

For investors considering the purchase of established residential properties, the inability to offset rental losses against employment income may significantly affect after-tax investment returns. Investors should carefully assess the tax implications before proceeding with any residential property investment.

2. Capital Gains Tax (CGT) Reform

The Government proposes significant changes to the CGT regime from 1 July 2027. The new rules will apply only to capital gains accrued after that date.

Key proposed changes include:

• Replacing the current 50% CGT discount with an inflation-indexed approach that taxes only real capital gains.

• Introducing a proposed minimum 30% tax rate on capital gains (subject to future legislative detail).

• Allowing investors in newly built residential properties to choose between the existing 50% discount method and the new inflation-indexation method.

3. Minimum Tax on Discretionary Trusts

From 1 July 2028, the Government proposes introducing a minimum tax rate of 30% on distributions made through discretionary trusts, subject to certain exceptions.

This measure is expected to significantly reduce the tax advantages associated with distributing trust income among lower-income adult family members.

Three-Year Restructuring Transition Period

To assist small businesses and families wishing to restructure their affairs, the Government proposes providing three years of rollover relief commencing from 1 July 2027.

Trust structures that may be affected should review their long-term succession and tax planning strategies well in advance.

4. Other Proposed Tax Measures

In addition to the above structural reforms, the Budget includes a range of measures aimed at simplifying compliance and supporting economic activity.

• A new $250 annual tax offset is proposed from the 2027–28 income year onwards.

• From 2026–27, eligible employees will be able to claim a standard deduction of up to $1,000 for work-related expenses without maintaining detailed substantiation records.

• From 2026–27, eligible companies will be able to carry current-year tax losses back against tax paid in the previous two income years.

• From 1 July 2026, the $20,000 instant asset write-off for eligible small businesses with annual turnover under $10 million is proposed to become a permanent feature of the tax system.

• From 2028–29, eligible start-up businesses operating for less than two years may be able to receive refunds for tax losses. Refunds will be capped by the amount of Fringe Benefits Tax (FBT) and PAYG withholding tax paid on employee wages.

• Electric Vehicle FBT Concessions:

From 1 April 2027, eligible electric vehicles valued above $75,000 will receive a permanent 25% Fringe Benefits Tax discount.

Eligible electric vehicles valued at $75,000 or less will continue to receive a full FBT exemption where the fringe benefit arrangement commenced before 1 April 2029.

As the 2025–26 financial year draws to a close, now is an ideal time to review your tax planning strategies.

Whether you are a property investor, hold assets through a family trust, or operate a small business, it is important to assess how these proposed reforms may affect your long-term financial and tax position.

Disclaimer

This article provides general information only and is based on proposals announced in the 2026–27 Federal Budget. At the time of publication, the measures remain subject to the legislative process and may change before becoming law.

This article does not constitute legal, taxation, or investment advice. You should seek advice from a registered tax agent or qualified professional adviser before making any financial or tax-related decisions.